The crushing weight of debt can feel like insurmountable pressure, making it seemingly impossible to get ahead financially. However, with focused effort, smart strategies, and a commitment to change, you can relieve that burden and continue on your path towards financial freedom.

This comprehensive guide provides seven practical techniques for assessing, prioritizing, and repaying debt in strategic ways while protecting and rebuilding your overall financial health. With a personalized approach, dedication to financial growth, and proven debt relief strategies, you can successfully eliminate debt and maintain lifelong financial discipline.

1. Completing a Comprehensive Debt Audit

The crucial first step is gaining complete clarity on your current financial situation by conducting a detailed debt audit. This involves tracking and cataloging every single debt you owe, including:

- Credit card balances

- Personal, auto, and student loans

- Mortgage debts

- Medical or utility bills

- Informal debts to friends/family

For each debt, note the following key factors:

- Original amount borrowed

- Current balance

- Interest rate

- Minimum monthly payment

- Total interest paid to date

- Fees or penalties

Recording this data in a spreadsheet, budgeting app, or written ledger provides tangible insights into what you owe and helps identify priority debts for repayment.

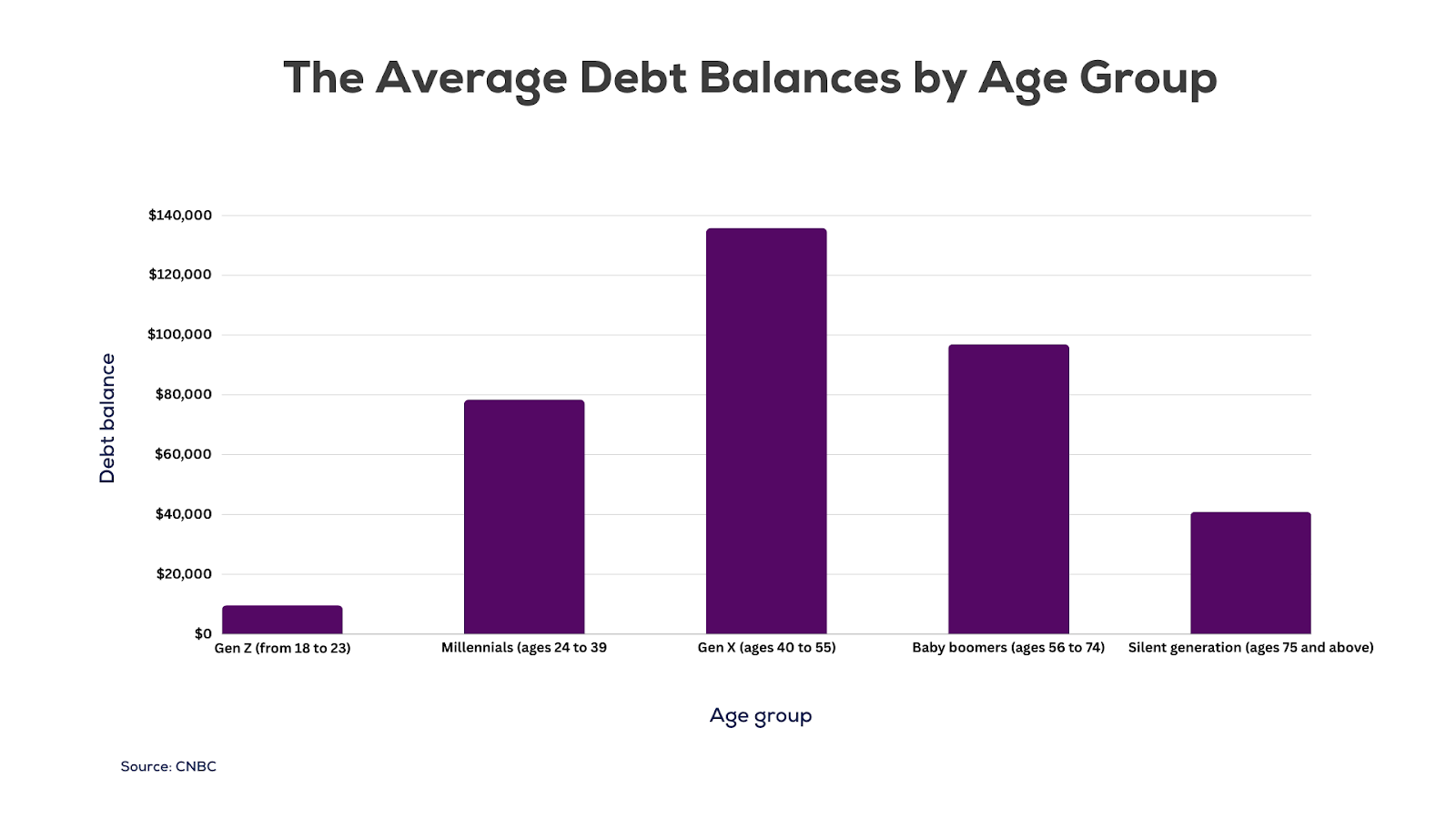

To benchmark against national averages, the chart below illustrates the average total balances outstanding by debt type and age demographic according to Experian’s annual consumer debt study:

As evidenced in the chart, younger demographics aged 18-35 have the highest credit card and student loan debt burdens, while those 36-64 carry the highest auto loan and mortgage debts. Retirees over age 65 have relatively low balances across all categories.

Understanding these age-based national debt trends can help you determine if your balances are significantly higher than peers, which can inform the aggressiveness of repayment prioritization. Likewise, realizing student loan and credit card debt tend to hit those under 35 hardest indicates getting ahead requires diligence around budgeting and lifestyle choices early on.

Armed with a comprehensive debt audit, you can understand your complete financial picture and create customized debt relief strategies.

2. Choose the Right Debt Repayment Strategy For You

With all debts cataloged and quantified, it’s time to strategically prioritize repayment in the most optimal order. Two popular methods are the debt snowball and debt avalanche:

Debt Snowball Method

The debt snowball method focuses on repaying the smallest debts first, regardless of the interest rate. This helps build momentum and motivation as you cross the smallest debts off your list first. However, higher interest debts continue to accumulate greater costs over time.

Debt Avalanche Method

The debt avalanche method prioritizes repaying the debts with the highest interest rates first, which reduces the overall cost of long-term borrowing. Using a debt avalanche method will save you the most in interest payments.

However, the sense of accomplishment in eliminating small debts quickly can be motivating. Choose the repayment strategy that best aligns with your financial personality and needs. Those with high credit card balances benefit more from the debt avalanche method.

3. Seeking Professional Guidance

When tackling debt, getting advice from financial professionals can provide an optimized financial strategy tailored to your situation. Financial advisors and credit counselors offer paid services to create personalized debt repayment and consolidation plans. They can also negotiate with creditors directly on your behalf.

Seeking consultations and guidance from financial experts can help create a debt freedom roadmap aligned with your unique financial situation and needs. Their experience navigating debt repayment success for others can be leveraged to accelerate your own financial journey.

For those in specific locations, local non-profit credit counseling services may be available. For example, for residents of New York struggling with debt, the high cost of living in New York City and surrounding areas leads many households to take on significant debt. New Yorkers dealing with debt may want to consider consulting with local non-profit credit counseling services for personalized guidance.

As New York residents struggle under burdensome high-interest debt, there are different new york debt relief programs offered in the state which provide critical financial counseling services to help people regain stable financial footing.By negotiating with creditors, these debt resolution providers can secure reduced interest rates or favorable settlement offers for their clients’ unsecured debts or obligations.

4. Debt Consolidation

Debt consolidation combines multiple debts into one new consolidated loan. The two types of loans used for debt consolidation are personal loans and balance transfer credit cards. Personal loans offer fixed interest rates and terms while balance transfer cards have variable rates but potentially 0% promotional APRs. Research both loan types to determine the best debt consolidation option for your situation.

Instead, you make one single payment towards the consolidated debt each month, reducing the administrative hassle. Debt consolidation also often lowers the average interest rate across the debts, saving money over the repayment period. This allows more of the monthly payment to go toward the principal rather than interest.

Research consolidation loans and balance transfer offers thoroughly to find reputable lenders and cards with the best terms for your situation. Look for low promotional rates, fees waived, and flexible limits. When done correctly, debt consolidation can lead to paying off debt years faster by simplifying payments and reducing interest costs.

5. Debt Negotiation

Calling up your various creditors directly to try to negotiate lower interest rates or waived fees can help reduce debt repayment costs. Explain your financial situation and desire to pay off the debt, but ask politely if they can reduce interest rates to assist you.

With credit card debts particularly, issuers want to retain reliable customers, so may agree to lower rates or waive annual fees if you have shown responsible usage and payments. Be persistent yet always polite when requesting rate reductions or any other concessions to ease your debt repayment path.

If a creditor verbally agrees to any reduced rates or waived fees, follow up and get it documented in writing before making further payments. This protects you in case an agreed upon concession is accidentally not applied later on. Overall, negotiating with empathy can lead to lowered burden and accelerated debt freedom.

6. Nonprofit Credit Counseling

If you need personalized guidance from a financial expert, nonprofit credit counseling provides customized debt management plans, consolidated payments, lower interest rates, waived fees, and budgeting advice.

Counselors conduct detailed evaluations of your full financial situation, then lay out step-by-step plans to optimally repay debts in 3-5 years through simplified payments. They can negotiate lowered rates and waived fees directly with your creditors on your behalf.

On average, nonprofit credit counseling clients complete debt repayment in 4-5 years, often significantly faster than trying DIY strategies. However, these services do come with enrollment fees, so compare costs across reputable providers. Evaluate your debt landscape, needs, and budget to determine if nonprofit credit counseling could optimize your path to freedom.

7. Create a Realistic Budget Prioritizing Debt

Alongside strategic repayment, a budget that frees up as much money as possible for debt elimination is crucial. Catalogue your average monthly income, then detail every expense, including:

- Housing costs

- Transportation

- Insurance

- Groceries

- Utilities

- Subscriptions

- Dining out

- Entertainment/leisure

Identify any non-essential costs that can be cut back or eliminated, such as excessive shopping or unused gym memberships. Shift these savings directly towards debt repayment. Apps like Mint, You Need A Budget, and EveryDollar can help track spending and model budget adjustments.

8. Increase Your Income to Accelerate Repayment

While minimizing expenses is vital, increasing your income opens up greater capacity to eliminate debt faster. Explore opportunities such as:

- Freelancing in your field of expertise

- Monetizing a hobby, skill, or talent

- Generating passive income through investing or real estate

- Seeking promotions and raises in your current role

- Finding a higher-paying job

Sell unused possessions collecting dust through garage sales, eBay, Craigslist, OfferUp, or Facebook Marketplace to convert clutter into cash flow. Limit excessive shopping and impulse purchases day-to-day to maximize financial capacity.

With extra income, remain diligent about allocating those funds directly to debt repayment until achieving freedom. Avoid lifestyle inflation or spending hikes.

9. Debt Settlement

If struggling severely to manage debt independently, trusted third party services provide options, but analyze risks thoroughly first:

Debt settlement companies negotiate reduced lump-sum payouts with creditors, often settling balances for 30-50% less than owed. However, this damages credit scores and taxes the forgiven debt.

10. Bankruptcy

As a last resort, bankruptcy liquidates assets to eliminate debt, but ruins credit scores for 10 years. Chapter 7 bankruptcy discharges unsecured debts while Chapter 13 restructures repayment over 3-5 years before discharging the rest.

Weigh outcomes carefully before pursuing settlement or bankruptcy. In many cases, consistent budgeting and repayment plans achieve debt freedom faster than these more damaging options.

11. Protect Credit Health While Paying Down Debt

As you pay off debts, routinely check your credit reports from Equifax, Experian and TransUnion for inaccuracies negatively impacting your score. Dispute any errors with included instructions.

On-time payments, diverse credit mix, and low utilization of credit limits gradually strengthen your score over time. Avoid closing old accounts since account history length is favorable.

Limit new credit card or loan applications until your credit score builds momentum. Initial hits to credit from strategies like debt settlement can be overcome through dedicated credit building. Be vigilant about protecting your credit throughout debt repayment.

12. Build an Emergency Fund

Once debt-free, immediately begin building an emergency fund covering 3-6 months of living expenses. Save this in a high-yield savings account as a buffer for income loss, medical bills, car repairs or other costly surprises.

According to Bankrate’s Financial Security Index Report, 56% of Americans cannot cover a $1,000 emergency with savings. Protect your post-debt freedom by saving rather than risking new debt.

13. Sustain Financial Vigilance Long-Term

Continuing healthy money management habits post-debt prevents sliding backwards. Seek ongoing financial education through reputable books, podcasts and courses to expand skills.

Review budgets, spending and financial strategies quarterly, adjusting and improving over time. Celebrate meeting milestones like fully funding emergency savings, but stay grounded in consistency and diligence.

Sustain motivation by reflecting on previous financial accomplishments and the peace of mind life without debt provides. Surround yourself with a community focused on positive financial growth.

Staying vigilant about financial health protects the freedom achieved through debt repayment and positions you for continued success.

14. Leverage Debt Repayment Apps

Debt repayment apps offer valuable tools to optimize and simplify paying off what you owe. Apps like Debt Payoff Planner centralize all your debts into one easy-to-use dashboard for tracking. You can input key details on each debt like balances, interest rates and minimum payments.

The app then creates a customized repayment calendar, projecting exactly when each debt will be satisfied based on your repayment abilities. Watching debts get crossed off as you make progress provides tangible motivation to stay consistent.

These apps also offer reminders when payments are due to help avoid missed payments and penalties. Overall, debt apps provide at-a-glance tracking, customized repayment projections, progress motivation, and payment reminders to help you crush your debt faster.

15. Reward Yourself for Milestones

Paying off debt requires sustained focus and sacrifice. While dedication is key, acknowledging milestones and achievements along the way provides positive reinforcement to stay on track. As you hit goals like paying off your first credit card or saving your initial emergency fund buffer, reward yourself in non-material ways, like a celebratory dinner out or weekend getaway.

Even small rewards like a movie night for finishing a repayment milestone reinforces the hard work you’ve accomplished. Just be sure rewards align with your budget and don’t counter debt repayment. An occasional non-material treat serves as a needed break and reminder of the progress you’ve made, lighting the fire to stay consistent on your journey to becoming debt-free.

Frequently Asked Questions

How many debt repayment strategies exist?

There are several proven strategies to become debt-free, including the debt snowball, debt avalanche, consolidation, negotiation, credit counseling, debt settlement, and bankruptcy. Evaluate your debt situation to choose the most optimal method.

What percentage of income should go towards debt repayment?

Financial experts recommend allocating 20-30% of your monthly take-home income specifically towards debt repayment. This aggressive savings rate helps pay off debt significantly faster.

How can I start increasing my income?

Options for earning extra income include freelancing, monetizing a skill or hobby, passive income through investing, real estate or blogging, promotion or new job negotiation, and selling unused items for cash flow. Every bit helps accelerate debt repayment.

Is debt consolidation advisable for credit card balances?

For those with numerous high-interest credit card debts, consolidation can simplify repayment through a single lower-rate balance transfer or loan, saving money. Research thoroughly to find the best terms.

What are the risks of debt settlement?

Debt settlement can seem appealing, but negatively impacts credit scores, collects hefty fees, and leads to tax liabilities for forgiven debt. Consistent budgeting and repayment often satisfies debts faster without settlement drawbacks.

How long does bankruptcy hurt your credit score?

Chapter 7 bankruptcy ruins credit scores for up to 10 years before improvement is possible through diligent credit building. Chapter 13 bankruptcy leaves a negative mark for 7 years post-discharge. Bankruptcy is a last resort with lasting consequences.

How do I stay motivated during my debt repayment journey?

Staying motivated is crucial to keep making continuous progress. Celebrate small wins like paying off the first credit card. Visualize your debt-free future. Join online communities for encouragement. Remind yourself daily why you started.

What should I do if I miss a debt payment due to financial hardship?

First, contact your creditors, explain the situation, and explore options like postponed payments. Avoid further missed payments through temporary budget cuts if possible. Consider debt counseling for customized debt management assistance.

Can I negotiate with my credit card company for lower interest rates?

Yes, you can call your credit card company and request a lower interest rate. Politely explain financial hardship and a desire to repay if they lower rates. If denied, wait 90 days and try again. Persistence combined with good standing can lead to lowered rates.

Should I use a debt repayment app to help manage the process?

Debt repayment apps like Debt Payoff Planner, Debt Destroyer, ReadyForZero, and Debt Manager can centralize information, create payment calendars, track progress, and motivate through the process. Leveraging tools optimizes repayment.

Conclusion

Starting a debt relief journey takes courage, discipline, and personalized strategies. While challenging, millions have succeeded repaying debt through focus and commitment. No matter your situation, implementing even a few steps in this guide can move you closer to freedom.

Debt relief is an ongoing process. Use this time to build habits and skills that will sustain your finances well into your debt-free future. With the right mindset and strategies, you can eliminate debt for good and achieve lasting financial wellness.